US Lenders for Secured & Unsecured Loans

After deciding whether a secured or unsecured loan is right for you, the next critical step is selecting a lender. The American financial landscape offers a wide array of institutions, each with its own set of advantages and disadvantages. These options range from large, traditional banks with a physical presence in nearly every city to member-owned credit unions and agile online-only lenders. Understanding the characteristics of each can significantly impact the interest rates, terms, and overall borrowing experience you receive. According to the Consumer Financial Protection Bureau (CFPB), shopping around among different types of lenders is a key strategy for finding the most favorable loan terms. The CFPB emphasizes that rates can vary widely, making comparison essential.

You will stay on this site.

Your choice of lender will depend on several factors, including your credit score, the amount you need to borrow, how quickly you need the funds, and whether you prefer digital convenience or in-person service. Large banks might be convenient for existing customers, while credit unions often prioritize member benefits, and online lenders focus on speed and accessibility. This guide will compare these popular options to help you determine the best fit for your secured or unsecured borrowing needs in the United States.

Major National Banks: Convenience and Broad Offerings

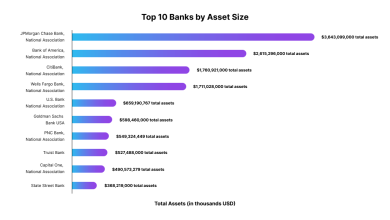

Large national banks like JPMorgan Chase, Bank of America, and Wells Fargo are often the first stop for many borrowers. Their primary advantage is convenience, especially for individuals who already have checking or savings accounts with them. These institutions offer a full spectrum of financial products, including both secured and unsecured loans. For secured options, they are major players in auto loans and Home Equity Lines of Credit (HELOCs). For unsecured lending, they offer personal loans, though their criteria can sometimes be stricter than other lenders. Relationship banking can be a benefit, as existing customers may sometimes receive preferential rates or a more streamlined application process. However, their size can also mean less flexibility in underwriting and interest rates that may not be as competitive as those from more specialized lenders.

Credit Unions: Member-Focused and Competitive Rates

Credit unions are non-profit, member-owned financial cooperatives. This structure is their defining feature and often translates into significant benefits for borrowers. Institutions like Navy Federal Credit Union and PenFed Credit Union are known for offering some of the most competitive rates on the market for both secured and unsecured loans. Because they serve their members rather than outside stockholders, profits are often returned to members in the form of lower interest rates on loans and higher dividends on savings. Recent market analysis frequently shows credit unions leading in low-cost auto and personal loans. They can also be more flexible with members who have less-than-perfect credit, taking a more holistic view of an applicant’s financial situation. The main requirement is membership, which is typically based on geography, employer, or affiliation with a particular group.

The Rise of Online Lenders

In the last decade, online lenders such as SoFi, LightStream, and Upstart have disrupted the personal loan market. Their business model is built on technology, allowing for a fully digital application, rapid decision-making, and often, funding within one or two business days. These lenders primarily specialize in unsecured personal loans, using advanced algorithms that can assess risk based on more than just a credit score, sometimes including factors like education and employment history. This can be beneficial for applicants with thin credit files but otherwise strong financial profiles. A review of online lenders highlights speed and convenience as their main draws. While they offer competitive rates, it’s crucial to check for origination fees, which some platforms charge to process the loan. Most online lenders do not offer traditional secured loans like auto loans, though some, like LightStream, do offer secured options for specific purposes.

Comparing Annual Percentage Rates (APR) Across Lenders

When comparing loan offers, the Annual Percentage Rate (APR) is the most important number to consider. It includes not only the interest rate but also any lender fees (like origination fees), providing a more complete picture of the loan’s total cost. Secured loans almost always have lower APRs than unsecured loans because the collateral reduces the lender’s risk. However, even within one loan category, APRs can vary significantly between banks, credit unions, and online lenders. For example, a borrower with a good credit score might find a 7% APR for an unsecured personal loan at a credit union, while a large bank might offer them 9%, and an online lender might offer something in between. According to the Federal Deposit Insurance Corporation (FDIC), consumers should always compare APRs from at least three different lenders to ensure they are getting a competitive deal.

When you’re shopping for a loan, you’re shopping for money. The price you’ll pay is the interest and fees. Different lenders can charge very different prices, so it pays to compare offers. Getting a loan is a big decision, so take your time to find the best deal for you.

Loan Terms, Fees, and Borrower Experience

Beyond the APR, consider the loan’s terms. This includes the repayment period, which can range from one to seven years or more. A longer term means lower monthly payments but more total interest paid over the life of the loan. Also, investigate any potential fees, such as origination fees, late payment penalties, or prepayment penalties (fees for paying the loan off early). Credit unions and some online lenders often distinguish themselves by having no prepayment penalties. The borrower experience is also a factor—do you prefer the face-to-face service of a bank or credit union branch, or the 24/7 digital access of an online platform? Your personal preference for service and support should play a role in your final decision.

Which type of institution is best for a borrower with bad credit?

Credit unions are often more willing to work with members who have lower credit scores, taking a more personalized approach to underwriting. Some online lenders also specialize in loans for borrowers with fair or bad credit, though the APRs will be significantly higher to offset the increased risk.

Do credit unions always offer better interest rates than banks?

Generally, credit unions have a reputation for offering lower rates on average because of their non-profit, member-owned structure. However, this is not a universal rule. A large bank may offer a promotional rate or a relationship discount that makes their offer more competitive, so it is always essential to compare.

How quickly can I get an unsecured loan from an online lender?

Speed is a primary advantage of online lenders. Many can provide a loan decision within minutes and deposit the funds into your bank account as soon as the next business day after you are approved and accept the loan terms.

Can I get a secured loan from an online-only lender?

While most online lenders focus on unsecured personal loans, some do offer secured options. For example, some platforms offer auto loan refinancing or loans secured by a vehicle title. However, the range of secured products is typically narrower than at a traditional bank or credit union.

Is it better to get a loan from a bank where I already have an account?

It can be more convenient, and you may be eligible for a “relationship discount” on the interest rate. However, you should not assume your bank will offer you the best deal. Always compare their offer with those from other institutions like credit unions and online lenders.

What is the main difference between a bank and a credit union?

A bank is a for-profit institution owned by stockholders. A credit union is a non-profit financial cooperative owned by its members. This structural difference often leads to credit unions offering more favorable rates and lower fees to their members.

What is an origination fee and do all lenders charge one?

An origination fee is a charge for processing and underwriting a loan, typically calculated as a percentage of the loan amount and deducted from the loan proceeds. Not all lenders charge one. Many credit unions and some banks and online lenders offer loans with no origination fees, which can make them a more affordable option.

Ultimately, the best lender for a secured or unsecured loan is the one that offers the most favorable combination of APR, terms, and fees for your specific financial profile. Whether it’s a national bank, a local credit union, or an innovative online platform, taking the time to shop around and compare multiple offers is the most reliable way to secure an affordable borrowing solution.

Conditions may vary; check official rules.

Sources: https://www.forbes.com/advisor/personal-loans/secured-vs-unsecured-loans/, https://www.bankrate.com/loans/personal-loans/secured-vs-unsecured-loans/